The Dow Jones Industrial Average (DJIA) index crossed the 40,000 point-level for the first time in history last Thursday and closed above this symbolic milestone the following day.

The recent rally in the DJIA and the other major US benchmark indices (namely the S&P 500 and the Nasdaq) has been fuelled by fresh data showing inflation is finally easing once again. This would allow the Federal Reserve to begin its long-awaited interest rate cuts expected as from September.

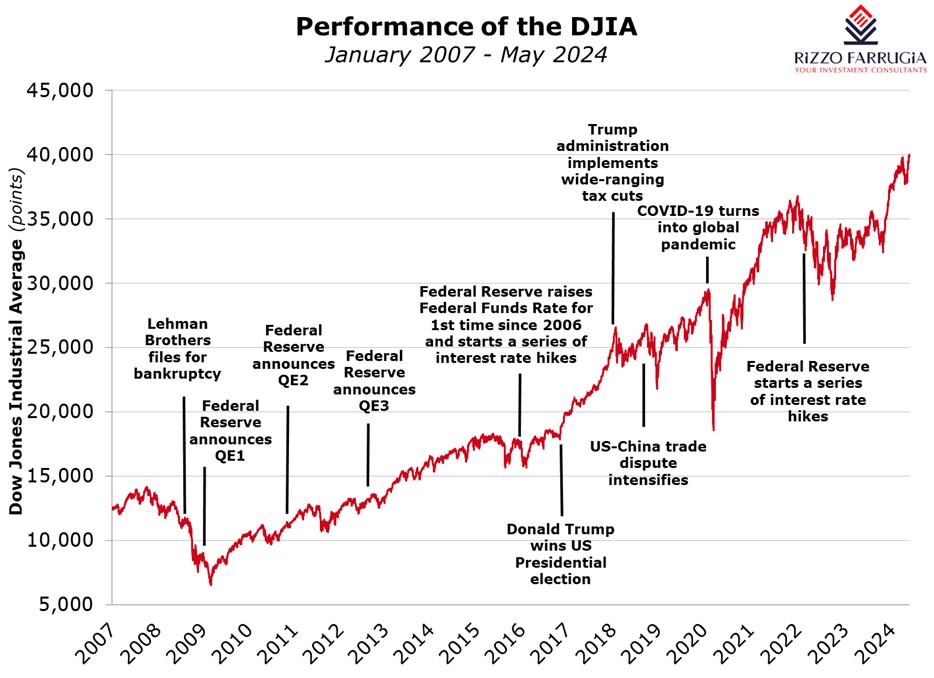

Although the DJIA is a price-weighted index as opposed to an index based on market capitalisation and therefore not a best representation of the largest companies within the US market, it is nonetheless interesting to monitor the major events over recent years since the DJIA first hit the 20,000-point milestone during the first week of Donald Trump’s presidency in January 2017.

After surpassing 20,000 points at the start of 2017, the DJIA index climbed by just under 50 per cent to a pre-pandemic high of just over 29,500 points in February 2020 but dropped back in a spectacular fashion with a decline of 38 per cent in a few weeks during the start of the pandemic to a low of 18,213 points recorded on 23 March 2020. The DJIA index then jumped by an extraordinary 65 per cent in eight months to above 30,000 points in November 2020 following the significant support from governments and central banks which boosted investor confidence. Earlier that month, Joe Biden had been elected to replace Donald Trump as US President.

The momentum from the lows achieved during the COVID-19 pandemic continued until the start of 2022 when the index hit a fresh all-time high of almost 36,800 points, representing a gain of just under 100% from its post-pandemic low in November 2020.

The bear market in 2022 resulted in the DJIA declining by 22 per cent to a low of 28,700 points in September 2022 as the Federal Reserve and other major central banks commenced a series of interest rate hikes. It has since jumped by 40 per cent in under two years despite a major pull-back between July 2023 and September 2023 at a time when the US 10-year treasury yield was hovering at a sixteen-year high of five per cent as the Federal Reserve hiked interest rates to their highest level since 2007.

The DJIA index therefore doubled in just over seven years from first reaching 20,000 points or just over four years when taking into consideration the more recent low in 2020.

This contrasts sharply with the previous milestones recorded by the DJIA as it had taken almost 18 years for the index to double from 10,000 points in March 1999 to 20,000 points in January 2017 in view of the sharp pullbacks registered during the ‘dot-com’ crash and the international financial crisis.

Although the DJIA index is given ample coverage by most mainstream business platforms, many financial journalists criticise the composition of the index since it is price-weighted. This means that the companies with the highest absolute share prices have a larger influence on the performance of the index.

Currently, the biggest constituents of the DJIA are UnitedHealth Group (which is the 15th largest company by market cap) and Goldman Sachs (the 63rd largest company by market cap). Together they are valued at about USD500 billion, but they have a larger influence on the index than some of the other constituents such as Microsoft (the third largest in the DJIA), Apple and Amazon.com combined, even though these three companies are valued at more than USD7.5 trillion combined.

Other notable companies within the DJIA that have a higher weighting compared to their market cap are Caterpillar Inc, The Home Depot Inc, Amgen Inc and Boeing.

Critics also highlight the fact that only three companies forming the so called Magnificent seven are included in the DJIA, namely Microsoft, Amazon and Apple. In fact, within the semi-conductor industry, the only constituent is Intel Corp having a market cap of USD136 billion while Nvidia Corp with a market cap of USD2.3 trillion and the third largest company in the S&P 500 has not yet been included in the DJIA so far.

In fact, due to the composition of the index and its lower weighting to the Magnificent seven and more to healthcare, financial and industrial companies, the DJIA is lagging behind the S&P 500 index by 5 percentage points so far this year. Moreover, since the low at the time of the pandemic in March 2020, the S&P 500 index increased by 140 per cent while the DJIA jumped by 115 per cent.

Nonetheless, the DJIA surpassing the 40,000-point level is still an important milestone indicating the strong performance of the US equity market. Following this important event for the DJIA last week, a prominent market commentator stated “The combination of the Fed likely to be lowering interest rates because inflation is moderating with a resilient economy is a beautiful scenario for a bull market.”

Historically, during periods of economic expansion, equity markets tend to perform very well. This trend is characterised by sustained growth in company profitability, increased consumer spending, and robust economic indicators.

Although invariably there will be periods of volatility and weakness in the markets similar to the downturn seen last month, a continued upward trajectory for equities is very likely over the near term.

In fact, historically, bull market cycles often last several years. The current bull market commenced in the fourth quarter of 2022 and since then the DJIA is up by almost 40 per cent. As explained in my article early this year, bull markets on average last more than four and a half years.

In this environment, investors must not be distracted by inevitable short-term pullbacks caused by a variety of factors including geopolitical tensions, unexpected economic data, or shifts in investor sentiment. It is important to maintain a long-term outlook where equities can produce substantial gains during a bull market cycle.

Read more of Mr Rizzo’s insights at Rizzo Farrugia (Stockbrokers).

The article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article.

Another takeover bid in Malta

Edward Rizzo says that one cannot exclude other takeovers taking place across the Maltese capital market in the near future

PG’s revenue approaches €200 million

Record revenue for PG plc as supermarkets and franchise operations continue to grow amid competitive pressures

The power of compounding

An investment of $100 into Berkshire Hathaway in 1965 would have grown to a current value of over €4.3 million